Weathering the Storm: Your Guide to Claiming Roof Damage

•

Written By

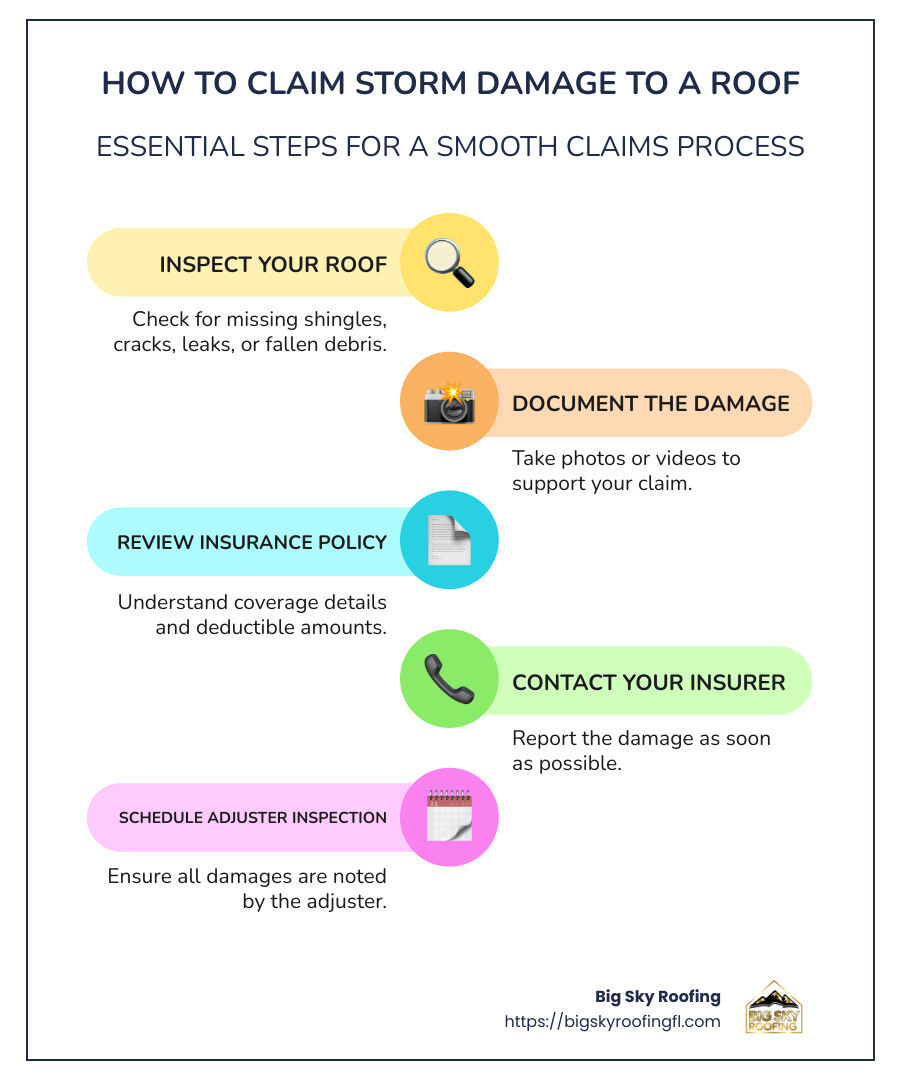

How to claim storm damage to a roof can feel overwhelming, but here’s a quick guide to get you started:

- Inspect Your Roof: Check for missing shingles, cracks, leaks, or fallen debris.

- Document the Damage: Take photos or videos to support your claim.

- Review Your Insurance Policy: Know the coverage details and deductible amounts.

- Contact Your Insurer: Report the damage as soon as possible.

- Schedule an Adjuster Inspection: Ensure all damages are noted.

- Choose a Trusted Contractor: Opt for someone experienced in storm damage and insurance claims.

In Florida counties like Sumter, Lake, Citrus, Hernando, Orange, and Marion, storm season is a regular concern for homeowners. Roof damage during these times can lead to significant stress, but understanding how insurance works can make the recovery process smoother. After a storm, the top priority is to ensure your roof remains intact, safeguarding your home and family from further harm. Insurance can be your ally, but only if you steer the claims process with care and diligence.

By following the steps outlined above, you can be better prepared to handle the aftermath efficiently, restoring your peace of mind and protecting your investment.

Understanding Your Insurance Policy

When it comes to homeowners insurance, understanding your policy can be the difference between a smooth claim process and a frustrating experience. It’s essential to know what your policy covers and how it operates, especially in storm-prone areas like Sumter, Lake, Citrus, Hernando, Orange, and Marion counties in Florida.

Replacement Cost vs. Actual Cash Value

Two key terms you’ll come across in your insurance policy are Replacement Cost and Actual Cash Value (ACV). These determine how much your insurance will pay if your roof is damaged.

Replacement Cost Coverage (RCV) pays for the cost to replace your roof at current market prices. This means if a storm damages your roof, your insurance will cover the costs to repair or replace it as if it were new, without deducting for depreciation. This is ideal for homeowners as it ensures you can restore your roof to its original state without significant out-of-pocket expenses.

On the other hand, Actual Cash Value (ACV) takes depreciation into account. If your roof is older or has signs of wear, the insurance payout will be less. The older your roof, the less you’ll receive, as the payout reflects the roof’s current value, not what it would cost to replace it new.

Why It Matters

Knowing whether your policy is RCV or ACV is crucial. As roofs age, some insurance companies might switch your coverage from RCV to ACV without much notice. This change can significantly impact the payout you receive when you file a claim. Always review your policy at renewal to stay informed about any changes to your coverage.

Deductibles and Coverage Limits

Another aspect to consider is your deductible—the amount you pay out-of-pocket before your insurance kicks in. Some policies have different deductibles for wind and hail damage, so you might pay more if your roof is damaged in a storm. Understanding these details can help you avoid surprises when filing a claim.

In the storm-prone regions of Central Florida, having a clear grasp of your insurance policy can save you time, money, and stress. By knowing your coverage type and deductible amounts, you can make informed decisions and ensure you’re adequately protected when the next storm hits.

How to Claim Storm Damage to a Roof

When a storm hits, it can leave your roof in shambles. Knowing how to claim storm damage to a roof is crucial for getting the repairs you need without breaking the bank. Here’s a step-by-step guide to navigating the insurance claim process.

Steps to File a Claim

- Contact Your Insurer Immediately: As soon as you’ve assessed the damage, call your insurance company. Provide a detailed description of the damage, and follow their instructions on the next steps. Quick action can prevent further damage and speed up the claim process.

- Document the Damage: Take clear photos and videos of all the damage. This evidence will be crucial for your insurance claim. Document everything, from missing shingles to leaks and structural issues. The more detailed you are, the better.

- Make Emergency Repairs: If your roof has leaks, cover them with a tarp to prevent further water damage. Keep receipts for any materials you purchase, as these may be reimbursed by your insurance company.

- Schedule an Adjuster Inspection: Your insurer will send an adjuster to assess the damage. During this inspection, provide all your documentation and be present to answer any questions. Having a contractor present can also help ensure nothing is overlooked.

- Review the Adjuster’s Report: Once the adjuster completes their inspection, they’ll provide a report. Review this carefully and ensure it matches your documentation. If there are discrepancies, discuss them with your insurer.

Types of Coverage: ACV vs. RCV

Understanding your insurance coverage type is key when filing a claim.

- Actual Cash Value (ACV) Policy

With an ACV policy, the insurance company pays the current value of your roof, factoring in depreciation. If your roof is old, the payout might be less than the cost of a new roof. This can mean more out-of-pocket expenses for you.

- Replacement Cost Value (RCV) Policy

An RCV policy covers the cost to replace your roof at current market prices, without depreciation deductions. Initially, you’ll receive a check for the ACV, and once repairs are completed, the insurer will pay the remaining amount to cover the full replacement cost. This type of policy is generally more favorable as it reduces your financial burden.

Why Coverage Type Matters

In storm-prone areas like Sumter, Lake, and Citrus counties, understanding whether your policy is ACV or RCV is crucial. It can significantly affect the amount you receive and your ability to restore your roof to its original condition after a storm.

By following these steps and understanding your policy, you can steer the claim process more effectively and ensure your roof is repaired or replaced with minimal stress. Next, we’ll explore the factors that can affect your claim, including deductibles and your claim history.

Factors Affecting Your Claim

Filing a claim for storm damage to your roof involves more than just picking up the phone. Several factors can influence how your insurance company evaluates and processes your claim. Understanding these can help you steer the process more effectively.

Deductible

Your deductible is the amount you’ll need to pay out-of-pocket before your insurance kicks in. If your deductible is $2,000 and the repair costs are $1,500, you won’t receive a payout. Even if the repair costs slightly exceed your deductible, you might decide against filing a claim to avoid potential rate hikes. Always weigh the cost of repairs against your deductible before making a decision.

Claim History

Insurance companies keep a close eye on your claim history. Filing too many claims in a short period can label you as a high-risk client, leading to increased premiums or even policy cancellation. Typically, one or two claims every ten years is considered normal. However, if you’re filing claims every year or two, your insurer might see this as a red flag. It’s crucial to reserve claims for significant, unavoidable damage, like storm-related roof damage, rather than minor issues you can handle yourself.

Roof Condition

The condition of your roof before the storm can significantly impact your claim. If your roof was already in poor shape, with visible wear and tear or pre-existing damage, your insurance company might deny your claim. They could argue that the damage resulted from inadequate maintenance rather than the storm.

In Florida counties like Orange and Marion, where storms are frequent, maintaining your roof is not just good practice—it’s essential. Regular inspections and maintenance can help ensure that your roof is in top condition, reducing the risk of claim denials due to negligence.

Understanding these factors can help you make informed decisions when filing a claim for storm damage to your roof. Next, we’ll discuss what to expect during the claim process, including the role of the adjuster and potential challenges you might face.

What to Expect During the Claim Process

When you file a claim for storm damage to your roof, be prepared for a journey that requires patience and diligence. Here’s what you can expect during the process:

A Long and Detailed Process

Many homeowners assume that once they file a claim, repairs will begin immediately. Unfortunately, that’s not the case. The insurance claim process is typically long and involves multiple steps and stakeholders. From contacting your insurer to the final approval, each phase can take time.

Why does it take so long?

- Multiple Steps: You’ll need to contact your insurer, document the damage, and possibly make emergency repairs to prevent further issues.

- Adjuster Inspection: An insurance adjuster will visit your property to assess the damage and determine the payout.

- Approval Process: Your claim will go through an approval process, which can involve back-and-forth communication between you, your contractor, and the insurance company.

The Role of the Adjuster

The adjuster plays a critical role in the claims process. This individual is responsible for inspecting your roof and determining the extent of the damage. They will assess whether the damage is covered under your policy and estimate the repair costs.

Key Points to Remember:

- Be Prepared: Have all your documentation ready, including photos and any repair estimates. This will help the adjuster make an accurate assessment.

- Communication is Key: Be clear and concise when discussing the damage with the adjuster. Avoid making statements that could be interpreted as admitting negligence.

Potential for Claim Denial

Despite your best efforts, there is always a possibility that your claim could be denied. Insurance companies may deny claims for several reasons:

- Pre-existing Damage: If your roof was already in poor condition before the storm, your claim might be denied.

- Inadequate Maintenance: Claims can be denied if the insurer determines that the damage was due to a lack of maintenance.

In Florida counties like Citrus and Hernando, where weather conditions can be harsh, it’s crucial to keep your roof well-maintained to avoid potential denials.

Knowing what to expect during the claim process can help you steer it more effectively. With patience and the right preparation, you’ll be better equipped to handle any challenges that arise. Next, we’ll address some frequently asked questions about claiming roof damage.

Frequently Asked Questions about Claiming Roof Damage

How to Claim Roof Damage from a Storm?

Filing a claim for storm damage to your roof can feel daunting, but breaking it down into simple steps can help.

- Contact Your Insurer: As soon as you notice damage, call your insurance company. They will guide you on the next steps and may suggest emergency repairs to prevent further damage.

- Document Everything: Take clear photos and videos of the damage. Gather any repair estimates or receipts for temporary fixes. This documentation is crucial for your claim.

- Schedule an Adjuster Inspection: Your insurer will send an adjuster to inspect the damage. Make sure you or your contractor are present to discuss the findings.

- Submit a Detailed Report: Provide a comprehensive report with all your documentation. This helps the adjuster make an accurate assessment and speeds up the process.

- Follow Up: After the inspection, keep in touch with your insurer. Be patient, as the process can take time.

What Not to Say to a Roof Insurance Adjuster?

When speaking with an adjuster, your words matter. Here’s what to avoid:

- Admitting Fault: Never say anything that could imply negligence, like “I should have fixed that earlier.”

- Speculating on Damage: Stick to the facts. Don’t guess about the cause or extent of the damage.

- Discussing Other Claims: Avoid mentioning past claims or other unrelated issues unless asked directly.

By being cautious with your words, you can prevent misunderstandings that might affect your claim.

Will My Homeowners Insurance Go Up if I File a Roof Claim?

Filing a claim can affect your insurance premiums, but it depends on several factors:

- Claim History: If you’ve filed multiple claims in recent years, your premiums might increase. Insurers view frequent claims as a higher risk.

- Type of Claim: Claims for unavoidable events, like storm damage, are less likely to impact your rates compared to avoidable incidents.

- Policy Details: Some policies offer “claim forgiveness,” meaning your first claim won’t affect your premium. Check your policy for specifics.

In counties like Marion and Lake, where storms are common, understanding these nuances can help you make informed decisions about filing a claim.

Maintaining your roof and keeping detailed records can aid in a smoother claims process. Next, we’ll conclude with final thoughts on navigating roof damage claims.

Conclusion

Navigating the storm damage claims process can be challenging, but with the right guidance, it’s manageable. At Big Sky Roofing, we pride ourselves on being a trusted partner for homeowners in Central Florida. With over 25 years of experience, our team is dedicated to providing superior craftsmanship and customer service.

Whether you’re in Sumter, Lake, Citrus, Hernando, Orange, or Marion County, our licensed and insured experts are here to help you through every step of the process. From assessing storm damage to working alongside your insurance company, we ensure your roof is restored to its best condition.

Our commitment to quality and integrity means you can trust us to handle your roofing needs with care and precision. We offer free estimates and emphasize clear communication, so you know exactly what to expect.

If you’re facing roof damage from a storm, let us help you weather the storm. Visit our services page to learn more about how we can assist you in restoring your home.